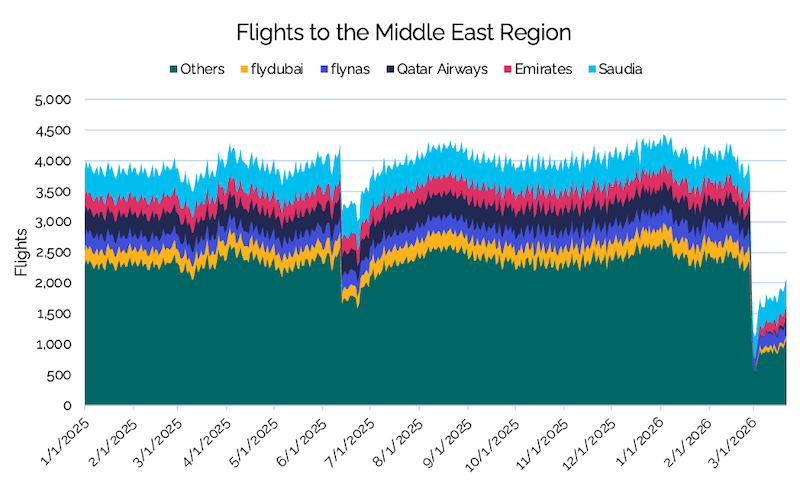

The widespread airspace closures that have taken place across the Middle East since 28th February, 2026 have resulted in a 59% reduction in all flights operating to, from, and within the region. This is based on IBA data that is accurate up to and including 22nd March, 2026.

IBA’s data shows that Middle Eastern carriers have been most affected, with Emirates reducing flights by 53%, equivalent to 3% of its annual operations. Qatar Airways has also cut almost its entire schedule in the period from 28th February to 22nd March, representing approximately 6% of its annual flights.

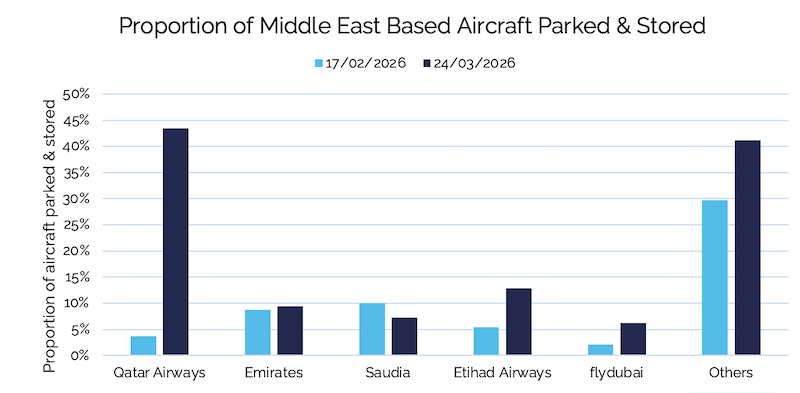

Intelligence from IBA also found that airlines operating through the region have been forced into longer routings, and increased flight times and operating costs. Some carriers have also begun placing aircraft into storage, with Qatar Airways parking approximately 43% of its fleet, as of 24th March, 2026.

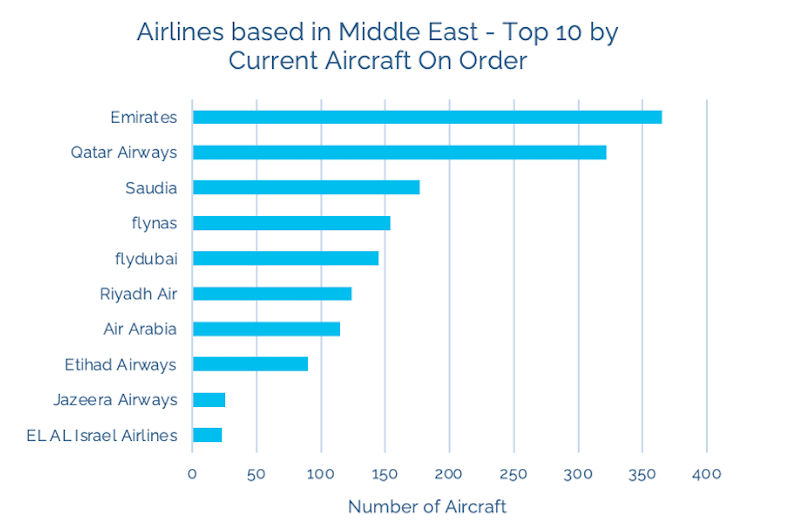

Despite the near-term disruption, IBA does not expect a material shift in long-term fleet strategies among Middle Eastern carriers. Airlines in the region remain well-covered for future growth and replacement, with aircraft order backlogs often exceeding the size of their current fleets, and more than 360 aircraft orders placed in 2025 alone.

Aircraft orders are based on long-term strategic planning, and we do not currently see a significant risk of cancellations. However, if disruption persists, we may see some deferrals of near-term deliveries.

At the same time, IBA data shows that sustained high oil prices are intensifying financial pressures on airlines, with jet fuel currently at approximately 118.8% of last year’s average (IATA figures). Fuel, which accounts for around 21% of total airline costs, has seen sharp increases that could reduce industry EBIT margins by approximately 3.5 percentage points, pushing weaker carriers towards loss-making territory.

IBA anticipates that in the short-term, the impact of higher fuel prices will be partially mitigated by airline fuel hedging strategies, although not all airlines have this facility. While airlines are expected to pass some of the costs through to consumers, with ticket prices potentially rising by up to 9% (IATA data), demand elasticity, particularly in leisure markets, may limit the extent to which higher costs can be passed on to passengers.

IBA expects that this environment is likely to widen the gap between financially stronger airlines and weaker operators, accelerating consolidation and increasing financial stress among carriers with limited access to capital. In response, airlines are expected to tighten capacity, prioritise higher-yield routes, and accelerate investment in more fuel-efficient aircraft.