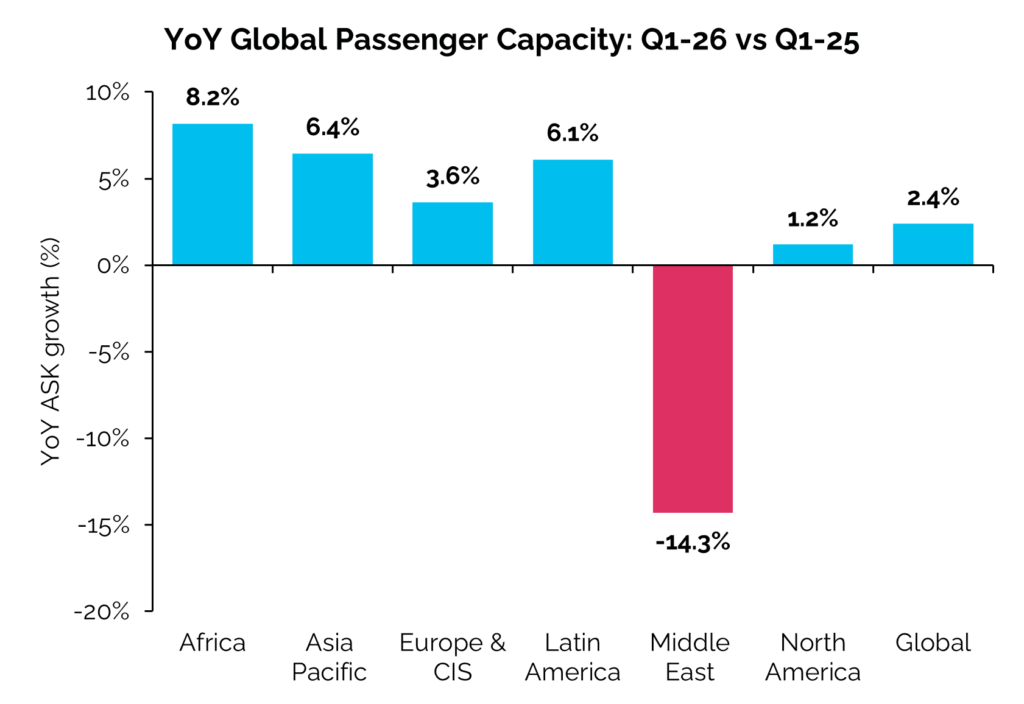

Analysis from the IBA aviation intelligence and advisory company shows that global airline passenger capacity grew by 2.4% year-on-year in Q1 2026, despite significant regional disruption. Capacity in the Middle East fell by 14% over the same period, as airspace closures and reduced operations weighed on international markets and constrained overall growth.

Most regions recorded solid expansion, with Asia, Europe, Latin America and Africa growing between 4% and 8% year-on-year. However, this was offset by weaker performance in North America, where capacity rose by just 1.2% to 611 billion Available Seat Kilometres (ASKs), highlighting a widening gap between higher-growth and more mature markets.

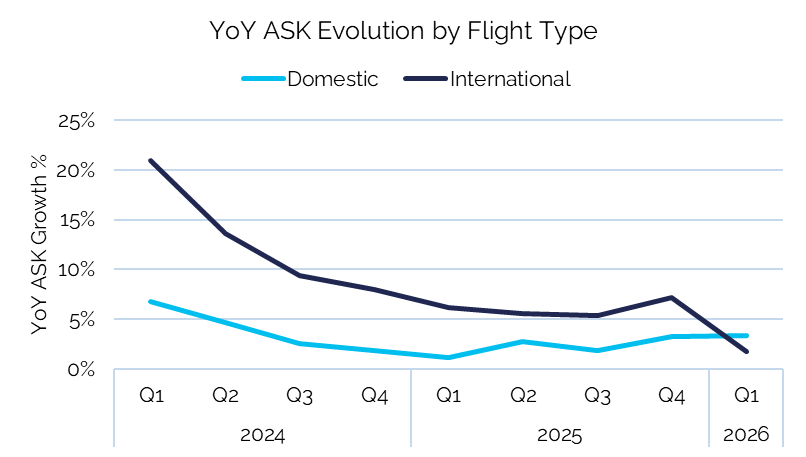

Domestic markets continue to drive the recovery, with capacity increasing by 3.3% year-on-year, compared to 1.7% for international travel. Domestic capacity is now 20% above 2019 levels, while international capacity growth over the same period is lower at 9.5%, reflecting a more gradual long-haul recovery.

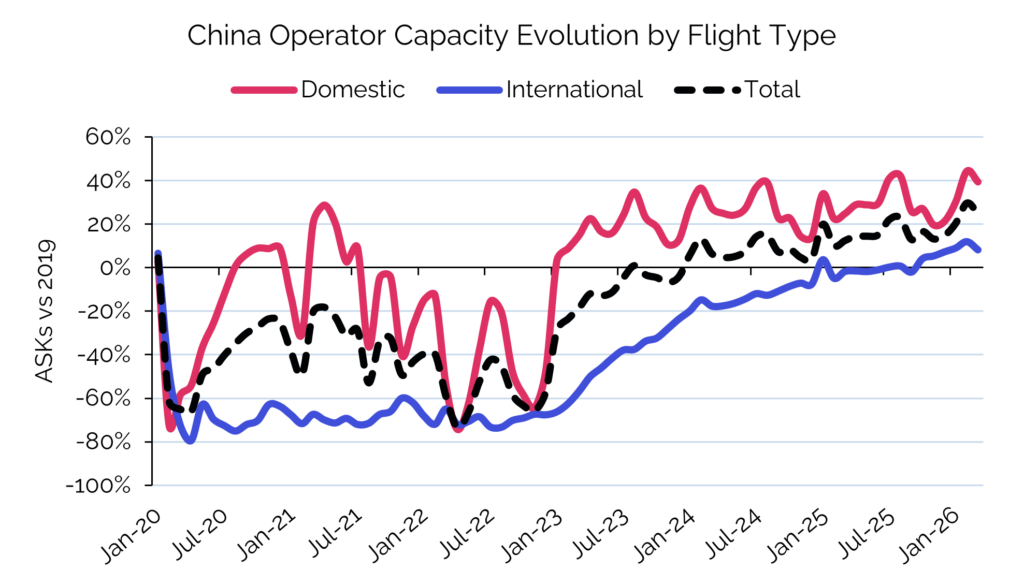

China remains a key growth driver, with capacity 9% above Q1 2025 and 25% higher than pre-pandemic levels. Strong domestic demand continues to underpin this growth, while international capacity has steadily recovered.

Supply constraints continue to limit expansion, with 271 aircraft delivered in Q1 2026, down 3% year-on-year, and 22% compared to 2018. Narrowbody aircraft deliveries are down 5% year-on-year at 215 aircraft for Q1 2026, with Airbus A320neo family deliveries averaging 27 aircraft per month in Q1 2026, compared with 38 per month for the Boeing 737 MAX.